Last February, I wrote an article about the consequences of a (then potential) Brexit for the auto makers who produce cars in the UK. Now that the British people have actually voted to leave the European Union, let’s see how the result of the upcoming break-up may influence the sales rankings in the European car market in the second half of 2016. I’ll first start with clarifying that even when the split-up is completed, which is expected to take at least 2 years, we at Left-Lane.com will continue to include UK car sales data within our EU reports, as these include the countries with which the EU has a free trade agreement (p.e. Switzerland and Norway), and we’ll have to assume that such an agreement will be struck with the UK as well. Of course, with the vote taking place June 23rd, the effects won’t be fully visible yet in the June sales figures, not in the least because there’s always a delay of a few weeks between a customer order and the actual delivery (and registration of a “sale”) of a car. However, the uncertainty preceding the actual vote may have caused private buyers to at least postpone their purchase, as the UK market, which grew by 3,2% in the first half of the year, stabilized at -0,8% in June and +0,1% in July.

Last February, I wrote an article about the consequences of a (then potential) Brexit for the auto makers who produce cars in the UK. Now that the British people have actually voted to leave the European Union, let’s see how the result of the upcoming break-up may influence the sales rankings in the European car market in the second half of 2016. I’ll first start with clarifying that even when the split-up is completed, which is expected to take at least 2 years, we at Left-Lane.com will continue to include UK car sales data within our EU reports, as these include the countries with which the EU has a free trade agreement (p.e. Switzerland and Norway), and we’ll have to assume that such an agreement will be struck with the UK as well. Of course, with the vote taking place June 23rd, the effects won’t be fully visible yet in the June sales figures, not in the least because there’s always a delay of a few weeks between a customer order and the actual delivery (and registration of a “sale”) of a car. However, the uncertainty preceding the actual vote may have caused private buyers to at least postpone their purchase, as the UK market, which grew by 3,2% in the first half of the year, stabilized at -0,8% in June and +0,1% in July.

Contrastingly, while the rest of Europe was in a sales crisis, the UK has been one of the strongest markets in Europe in recent years, breaking sales records year after year as a result of low interest, a booming housing market and carmakers willing to offer good deals in one of the very few markets with an actual demand. However, the financial uncertainty of the coming few years during the break-up with the EU, combined with a depreciating British Pound are likely to stall that growth in the short and mid-terms, and analysts expect a decline of the British car market this year and next. In contrast, Southern European car markets had been hit exceptionally hard with a huge drop in sales after the global financial crisis since 2008, and they’ve only just started to accelerate their recovery from their rock-bottom crisis levels. Italy, Spain and France have been among the fastest growing countries in Europe in recent months, showing double digit gains over 2015 volumes. But the Brexit vote is also expected to temper those recoveries, as analysts have lowered their predictions of growth for the second half of 2016 for all of Europe, as the decline in the UK will not only influence the figure for the entire market, being the second-largest of the continent, but the uncertainty that comes with the break-up will also slow down growth in the rest of Europe.

So which brands are likely to suffer the most from a slowdown in the UK car market? The British brands Aston Martin, Bentley and Jaguar sell over half of their European volume in their home market, compared to an average of 17,7%, but the former two are low-volume brands and the third is enjoying an impressive revival with two important new products in showrooms this year. Looking at the top-25 best selling brands in Europe, those who sold more than 60.000 vehicles in the first half of 2016, we find two more British brands at the top: Land Rover with 46,2% of European sales registered in the UK and Mini with a 37,6% share, closely followed by Honda, which produces most of its vehicles for the European market in Swindon, UK. That also explains Nissan’s 5th place, until 2013 the biggest car producer in the UK. But the really big boys are Ford and Vauxhall, with over 171.000 and 133.000 UK sales respectively in the first half of 2016, which comprises 30,3% of Ford’s European volume and 24,8% for the General Motors division. These two brands are set to lose the most volume from a declining British market, just at the moment both of these European divisions of American manufacturers had started to make their first profits in the continent in over a decade.

So which brands are likely to suffer the most from a slowdown in the UK car market? The British brands Aston Martin, Bentley and Jaguar sell over half of their European volume in their home market, compared to an average of 17,7%, but the former two are low-volume brands and the third is enjoying an impressive revival with two important new products in showrooms this year. Looking at the top-25 best selling brands in Europe, those who sold more than 60.000 vehicles in the first half of 2016, we find two more British brands at the top: Land Rover with 46,2% of European sales registered in the UK and Mini with a 37,6% share, closely followed by Honda, which produces most of its vehicles for the European market in Swindon, UK. That also explains Nissan’s 5th place, until 2013 the biggest car producer in the UK. But the really big boys are Ford and Vauxhall, with over 171.000 and 133.000 UK sales respectively in the first half of 2016, which comprises 30,3% of Ford’s European volume and 24,8% for the General Motors division. These two brands are set to lose the most volume from a declining British market, just at the moment both of these European divisions of American manufacturers had started to make their first profits in the continent in over a decade.

Finally, it’s also interesting to see that the German luxury brands have a relatively high share of British sales, all three are above 20% after having successfully gained market share in the UK in recent years and regularly having one or more of their vehicles each in the models top-10.

| Brand | 2016-H1 UK sales | 2016-H1 EU sales | UK share |

| Land Rover | 42.559 | 92.086 | 46,2% |

| Mini | 33.963 | 90.220 | 37,6% |

| Honda | 32.449 | 88.685 | 36,6% |

| Ford | 171.192 | 564.716 | 30,3% |

| Nissan | 78.582 | 297.468 | 26,4% |

| Opel/Vauxhall | 132.947 | 536.821 | 24,8% |

| BMW | 91.610 | 423.891 | 21,6% |

| Mazda | 26.381 | 126.555 | 20,8% |

| Mercedes-Benz | 88.603 | 425.394 | 20,8% |

| Audi | 89.521 | 441.786 | 20,3% |

| Kia | 46.343 | 229.159 | 20,2% |

| Suzuki | 19.944 | 101.530 | 19,6% |

| Hyundai | 48.077 | 257.774 | 18,7% |

| Total | 1.420.636 | 8.018.411 | 17,7% |

| Toyota | 54.504 | 314.653 | 17,3% |

| Mitsubishi | 10.544 | 63.699 | 16,6% |

| Volvo | 22.629 | 148.370 | 15,3% |

| Seat | 24.634 | 180.632 | 13,6% |

| Skoda | 42.233 | 345.397 | 12,2% |

| Citroën | 37.781 | 309.409 | 12,2% |

| Volkswagen | 109.566 | 902.063 | 12,1% |

| Peugeot | 54.776 | 477.657 | 11,5% |

| Fiat | 33.324 | 414.042 | 8,0% |

| Renault | 44.570 | 592.226 | 7,5% |

| Dacia | 13.445 | 219.669 | 6,1% |

European brand ranking consequences

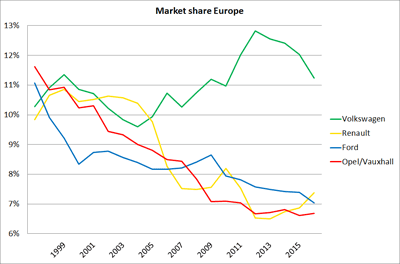

In September 2014, I published an article on the battle for second place in the European car brand ranking behind Volkswagen. Ford has held this position for 7 of the last 8 years including every year since 2011, but Renault and Opel/Vauxhall have been closing in lately as a result of overhauling their product line-up while Ford has had some delays in bringing new and updated models to the market. In that article I concluded that Renault would have the best shot at reclaiming the #2 spot it last held in 2010, as its new design language has been well received and it will have one of the freshest product line-ups in the industry by the end of this year. At that time, after Q3 of 2014, Renault trailed Ford by almost 100.000 units year-to-date: 747.000 vs. 653.000, with Opel/Vauxhall not far ahead at 680.000 sales. Fast forward 21 months and Renault has already passed Ford for the YTD #2 position in Europe thanks to a stellar performance in May and June. The French brand looks set to continue that momentum, though unlikely with the double digit growth figures it showed in these last two months. The Brexit vote has only fortified its position, taking into account the high dependence on the British market for both Ford and General Motors, especially compared with the French brand, which has benefited from the strong recoveries in the Southern European countries.

In September 2014, I published an article on the battle for second place in the European car brand ranking behind Volkswagen. Ford has held this position for 7 of the last 8 years including every year since 2011, but Renault and Opel/Vauxhall have been closing in lately as a result of overhauling their product line-up while Ford has had some delays in bringing new and updated models to the market. In that article I concluded that Renault would have the best shot at reclaiming the #2 spot it last held in 2010, as its new design language has been well received and it will have one of the freshest product line-ups in the industry by the end of this year. At that time, after Q3 of 2014, Renault trailed Ford by almost 100.000 units year-to-date: 747.000 vs. 653.000, with Opel/Vauxhall not far ahead at 680.000 sales. Fast forward 21 months and Renault has already passed Ford for the YTD #2 position in Europe thanks to a stellar performance in May and June. The French brand looks set to continue that momentum, though unlikely with the double digit growth figures it showed in these last two months. The Brexit vote has only fortified its position, taking into account the high dependence on the British market for both Ford and General Motors, especially compared with the French brand, which has benefited from the strong recoveries in the Southern European countries.

Renault is much less dependent on the British market than its two main rivals are. In fact, the French brand and its Romanian budget-brand are at the bottom of the ranking for dependence on the UK market, at a mere 7,5% of total European sales for Renault. Fiat is also below 10%, followed by the PSA brands and, surprisingly, Volkswagen, despite selling over 100.000 cars in the UK in the first six months of 2016. The other mainstream VW Group brands Seat and Skoda are also sell a relatively low share of their European volume across the Channel. For these brands and others that are below the average of 17,7%, a softening demand from British car buyers as a result of the Brexit uncertainty will have less influence on their overall European performance.

Of course, even though the UK is the second largest car market in Europe and has a disproportionate share of the European sales of some brands, its fortune will only have a limited influence on a brand’s performance. The life cycles of important models has a greater influence on the sales of the brand as a whole, as Renault has proven with its recent resurrection after a complete overhaul of its product portfolio. It will continue its momentum with the Megane and Talisman still in start-up mode, and the new generations of the Scenic and Koleos coming up. In contrast, Ford has been in the low-end of its cycle, with the Fiesta ready to be renewed by the end of this year and the Focus in its sixth year of the current generation. Opel/Vauxhall is also building momentum with the new Astra in showrooms and new generations of the Insignia, Meriva and Zafira coming up. And with such a close battle between these three brands, those lost UK sales can still make a difference between 2nd or 4th position in Europe.

Of course, even though the UK is the second largest car market in Europe and has a disproportionate share of the European sales of some brands, its fortune will only have a limited influence on a brand’s performance. The life cycles of important models has a greater influence on the sales of the brand as a whole, as Renault has proven with its recent resurrection after a complete overhaul of its product portfolio. It will continue its momentum with the Megane and Talisman still in start-up mode, and the new generations of the Scenic and Koleos coming up. In contrast, Ford has been in the low-end of its cycle, with the Fiesta ready to be renewed by the end of this year and the Focus in its sixth year of the current generation. Opel/Vauxhall is also building momentum with the new Astra in showrooms and new generations of the Insignia, Meriva and Zafira coming up. And with such a close battle between these three brands, those lost UK sales can still make a difference between 2nd or 4th position in Europe.