Last year BYD sold more New Energy Vehicles/NEVs than any other company in China. According to a ranking of the Top Twenty Selling NEVs in China, BYD sold more EVs and PHEVs than any other manufacturer. Cumulatively, the company sold 205,800 NEVs and dominated the list (see below) by placing 2nd, 4th, 6th, 8th, and 9th among the top twenty.

-

Top 20 Selling EVs/PHEVs in China

December 2018 and 2018 (full year)

China

December

2018

%

1

BAIC-EC Series

8407

90637

8

2

BYD Quin PHEV (Gen I and II)

4654

47424

4

3

JAC iEV S/E

6818

46586

4

4

BYD e5

8234

46213

4

5

Chery eQ

4732

39374

4

6

BYD Song PHEV

4544

39318

4

7

BAIC EU-Series

12561

37343

3

8

BYD Tang PHEV (Gen. I & II)

6807

37146

3

9

BYD Yuan EV

8021

35699

3

10

SAIC Roewe Ei6 PHEV

1473

33347

3

11

BAIC EX-Series

6844

32810

3

12

JMC E200

4846

31750

3

13

Geely Emgrand EV

2808

31426

3

14

Hawtai EV160

680

29731

3

15

SAIC Roewe Ei5 EV

3301

26008

2

16

SAIC Baojun E100

4692

25888

2

17

SAIC Roewe eRX5 PHEV

575

22711

2

18

Donfeng Junfeng Skio

4104

19226

2

19

Zotye E200

2293

18865

2

20

Hawtai xEV

1878

17776

2

Others

84991

410873

37

Total

181385

1102375

100

BYD’s best sellers included two sedans, the Quin PHEV and the more recently launched e5 450, also known simply as the e5. The price of a Quin PHEV in China is about 185,900 RMB ( approx. $27,600). With a top speed of 185 km/h (115 mph) and the ability to accelerate from 0-100 km/h in just under 6 seconds, the Quin PHEV (pictured below) does not lack in terms of power. When running purely on its 13kWh battery, the sedan has a maximum range of 70 kms.

Inside the car is a 12.3 inch screen with access to navigation systems, multimedia entertainment, and real time fuel economy information.

A number of convenience factors are built in, including smart-key functionality, tire pressure monitoring, and the ability to remotely control the car from outside the vehicle – – for example – – in low speed mode, while positioning or guiding the car into a parking space.

A number of convenience factors are built in, including smart-key functionality, tire pressure monitoring, and the ability to remotely control the car from outside the vehicle – – for example – – in low speed mode, while positioning or guiding the car into a parking space.

BYD’s other best seller is the e5, a pure (battery only) EV sedan which was originally launched at the 2015 Shanghai motor show. Partly because of its affordability, the e5 has been a popular choice among taxi cab operators.

The “after subsidies” price of the e5 in China is 140,000 RMB (approximately $20,760). The sedan has a fairly long range of 405 km. (253 miles) and a maximum speed of 130 km/h or 81 mph. The battery capacity is 60.48 kWh, and can be fast-charged to an 80% level in 90 minutes.

Inside is a fairly small touch screen, allowing access to the navigation system, multimedia entertainment, internet connectivity, etc.

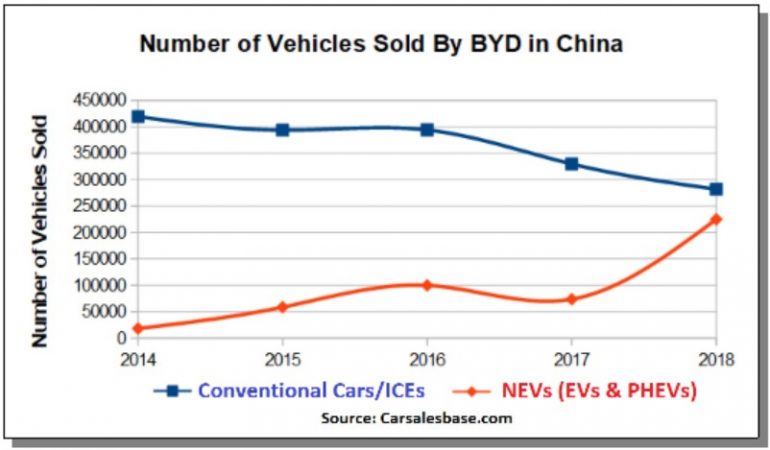

BYD is a pioneer in China’s NEV industry, yet is often known by Westerners as “the Chinese Electric Vehicle company that Warren Buffet has invested in.” The company makes both NEVs as well as conventional cars (i.e. cars powered by the Internal-combustion engine/ICE). For the year 2018, BYD sold more conventional cars in China (281,991) than NEVs (225,136), however, the gap between these vehicle types is closing. Last year represented a major rise in the number of New Energy Vehicles sold by BYD, while sales volume for conventional cars continued to drop, as can be seen in the graph below.

BYD is a pioneer in China’s NEV industry, yet is often known by Westerners as “the Chinese Electric Vehicle company that Warren Buffet has invested in.” The company makes both NEVs as well as conventional cars (i.e. cars powered by the Internal-combustion engine/ICE). For the year 2018, BYD sold more conventional cars in China (281,991) than NEVs (225,136), however, the gap between these vehicle types is closing. Last year represented a major rise in the number of New Energy Vehicles sold by BYD, while sales volume for conventional cars continued to drop, as can be seen in the graph below.

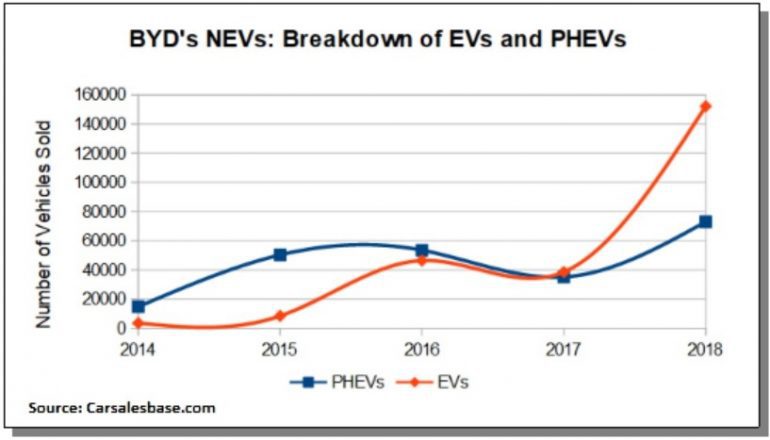

Within the NEV category it is also interesting to look at the breakdown between EVs and PHEVs, to get a better understanding of growth rates and trends. During the last two years, pure electric vehicles have surpassed Plug-In Hybrid Electric Vehicles (PHEVs), as a percentage share of BYD’s NEVs sold. The growing importance of pure electric vehicles (EVs) can be seen in the graph below.

From a more macro perspective, this year (2019) marks a major development for the automobile industry in China because car manufacturers will be required to comply with new government policies and regulations designed to address air pollution, carbon emissions, and global warming. This will have major implications not only for BYD, but for all manufacturers in terms of their production, and more specifically, the mix of their output in terms of ICEs and NEVs produced. For an excellent overview and explanation of what the new policies and regulations mean for the industry and manufacturers, readers will want to consult the Bloomberg quicktake article “China is About to Shake Up the World of Electric Cars.” In short, manufacturers will have three choices:

- produce more NEVs to meet quotas, that are specific to each manufacturer, as determined by the new regulations,

- don’t meet the quotas but comply with the policy by purchasing carbon-credits from other NEV producers (i.e. competitors) whom have earned surplus carbon credits,

- face stiff and costly fines and penalties for doing neither 1) nor 2) above.

BYD, as a long established leader in China’s NEV market is well positioned to not just comply with the new government policy and regulations, but to generate substantial revenues from selling its surplus carbon credits on the carbon market. Such revenues would be particularly valuable to a company like BYD, or any manufacturer for that matter, because they contribute directly to the company’s bottom line profits and corporate value.

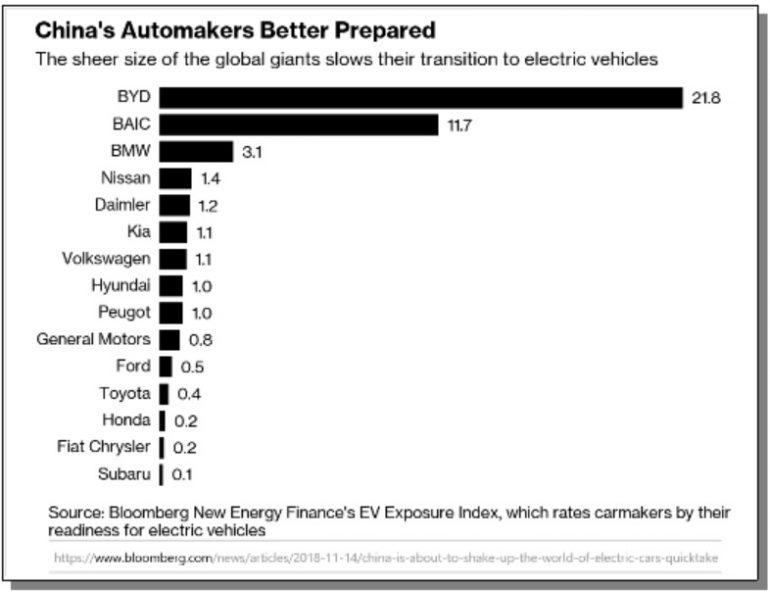

Within the context of China’s new policies and regulations, not all manufacturers are so well positioned as BYD. As seen in the Bloomberg graphic below some of the giants of the industry, for example Toyota, Ford, and General Motors; appear much less prepared. The score shown below is an EV Exposure Index, created by Bloomberg’s New Energy Finance team, which “rates car makers for their readiness for electric vehicles”.

BYD’s success producing and selling NEVs extends beyond sedans, SUVs, crossovers, etc.; or what we normally think of with regards to “passenger vehicles”. One area where BYD has been particularly successful is in the bus business, and more specifically producing and selling electric buses. BYD has delivered more than 35,000 electric buses globally, and has factories around the world in countries such as the UK, France, Hungary, Brazil, and the US.

Financially, 2018 has been a difficult year for BYD. Although full year 2018 financial results are not yet reported, based on BYD’s 2018 Third Quarterly Report here, it is clear that relative to 2017; profits for 2018 will be significantly lower.

BYD attributed lower expected profits to intense competition, as well as lower government subsidies, according to a Reuters article, which noted that 2018 profits could fall by about a third compared to the previous year.

Despite these challenges, BYD as a company ended its third quarter of 2018 sounding enthusiastic and bullish about its NEV business, and its future. BYD’s third quarter report included a “Forecast on the Results of Operations in 2018”. Below is an excerpt from that forecast:

-

The new energy vehicle business of the Group is expected to continue to maintain strong growth and drive the rapid recovery of the profits of the Group in the fourth quarter. In respect of new energy passenger vehicle segment, new models have accumulated a large amount of orders relying on their strong market competitiveness and their sales are expected to record significant increase compared with the same period of last year due to the easing of battery capacity bottlenecks.

Battery capacity bottlenecks, appears to be a reference to BYD’s battery supply chain, which it continues to invest heavily in. These investments involve not only new battery plants and factories, but also the rights to a guaranteed supply of lithium, from mining operations. Consider the following:

-

In January of 2018 Chinese media outlet Xinhua reported that BYD has signed a deal with a mining operation in Qinghai province to secure a supply of 30,000 tonnes of lithium carbonate.

-

In June of 2018, BYD’s opened its third battery plant, also in Qinghai province. The plant’s annual capacity is 10 GWh. The cost of BYD’s new factory is 4 billion RMB, or approximately $633 million dollars.

-

In August of 2018, BYD signed an agreement with the local government of Chongquing in Southwest China, to build a new battery plant at a cost of approximately 10 billion yuan, or $1.5 billion dollars. The Chongquing plant will have an annual capacity of 20GWh.

-

In September of 2018, BYD announced its plan to build yet another battery factory in Xi’an, the capital of Shaanxi province. The annual capacity of this facility will be 30GwH, according to an article here, by electrive.

-

With the three new battery plants referred to above, BYD will have a total of five battery plants in China, making the company a major player in the battery business.

-

In addition to BYD, the other major Chinese owned battery manufacturer competing for dominance in China is Contemporary Amperex Technology/CATL, which like BYD, has been growing in leaps and bounds in terms of its new or planned battery manufacturing capacity. BYD is planning to reach a total capacity of 60 GWh by 2020, while the corresponding figure for CATL is even higher at 88 GWh.

Benchmark Minerals, a company that specializes in the lithium ion battery supply chain

has recently produced an excellent analysis that poses the following rhetorical question: Who is Winning the Global Lithium Ion Battery Arms Race?

has recently produced an excellent analysis that poses the following rhetorical question: Who is Winning the Global Lithium Ion Battery Arms Race?

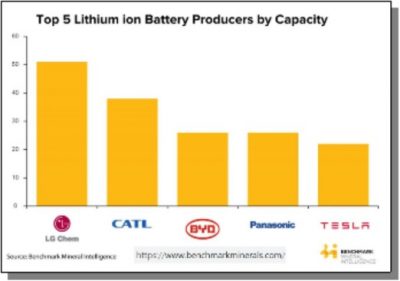

The graph to the left shows the Top Five Lithium ion Battery Producers by Capacity. Both CATL and BYD rank 2nd and 3rd respectively – – behind South Korea’s LG Chem, the global front-runner – – and ahead of Japan’s Panasonic and America’s Tesla – – two better known name-brand competitors.

Although most of the batteries produced by BYD’s factories will likely be inputs into its own cars, some of these same factories will also be supplying other automobile manufacturers – – including BYD’s real or potential competitors. For example, in March of 2018 BYD announced that it would be supplying Changan Auto, as reported here, in an Automotive News China article.

Much of the content above suggests that BYD will continue to ramp up its production and sales of New Energy Vehicles. Given the dynamic and innovative nature of the company, BYD will undoubtedly be an interesting player to watch during 2019, and well beyond.

For a complete list of sources and references used in this article; click here.

Full disclosure: I currently do not own shares in BYD, or any other company mentioned in this article.